26 November 2016 – 26 February 2017

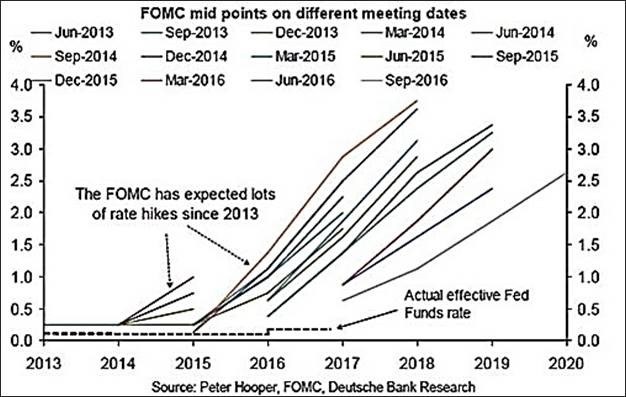

The FOMC has consistently overestimated future Fed Funds Rate (FFR) hikes. For a body that prides itself on super-scientific research methods and has teams of economists (self-described) and statisticians, it’s interesting that they can’t even predict their own behaviour.

The graph is comical.

These errors can be either unintentional or intentional.If unintentional, they are super-optimistic that just a few more months of a near-zero FFR will stimulate spending and employment figures enough to justify the future FFR increases. Also, this would mean that their models are junk. If intentional, they are just trying to project optimism, ever-reliant on the announcement effect. The announcement effect, however, can fade like in the story of the boy who cried wolf.

… My interpretation of these errors is [that if] unintentional, they represent economic ignorance; if intentional, they are an admission that they are powerless to bring about the economic recovery they have wanted to put in their trophy case for almost ten years now. Either way, in the fable, the villagers stopped believing the lying little boy one day

Jonathan Newman

The Fed Who Cried Growth (10 October 2016)

John Maynard Keynes as an Investor-Speculator:

A More Balanced Assessment

John Maynard Keynes (1st Baron Keynes of Tilton, 1883-1946) is usually remembered as the author of The General Theory of Employment, Interest and Money (1936) and the father of “Keynesian economics.” He was probably the most famous and influential – and certainly the most destructive – economist of the 20th century. Only infrequently, in contrast, has he been recalled as a speculator who lost heavily, learnt hard lessons and became an investor. One of today’s most prominent Keynesians, Paul Krugman, apparently didn’t know until John Wasik (the author of Keynes’s Way to Wealth, McGraw-Hill, 2014) informed him that Keynes managed several investment vehicles – one of which he ran into the ground.

To read the full Newsletter (PDF), click here.

![]()

[…] 2016, I reanalysed data compiled by Chambers, Dimson and Moggridge (see the attached pdf, which provides details, references, etc.). Unlike the academics, I analysed Keynes’s personal […]